The Greenhouse Gas (GHG) Protocol has been and continues to be the foundation of corporate climate disclosure. It’s now set to roll out updated climate reporting standards by 2027 – with major revisions planned for the Corporate Standard, Scope 2 Guidance, Scope 3 Standard, and related guidance on Actions and Market Instruments.

Summary

-

Major GHG Protocol updates are coming by 2028, with key revisions to Scope 1–3 standards and new guidance on land use, market instruments, and removals, reshaping emissions reporting globally.

-

Stricter rules will improve data consistency, close loopholes, and align with IFRS S2 and CSRD, reducing interpretive flexibility and increasing comparability across companies.

-

Scope 3 and carbon market claims will face scrutiny, requiring better data, supplier engagement, and credible use of carbon credits and RECs for investor trust and target-setting.

-

CFOs and CSOs should prepare early by auditing current practices, involving the board, investing in data quality, and tracking draft releases to stay ahead of evolving compliance expectations.

This update to the GHG Protocol is like an overhaul of international accounting standards, and it will reshape how companies account for and report their greenhouse gas emissions.

This is a reset of the global baseline for credible, comparable, and compliant emissions footprints. Here’s what this timeline looks like.

Consider it a progressing reset of the global baseline for credible, comparable, and compliant emissions footprints.

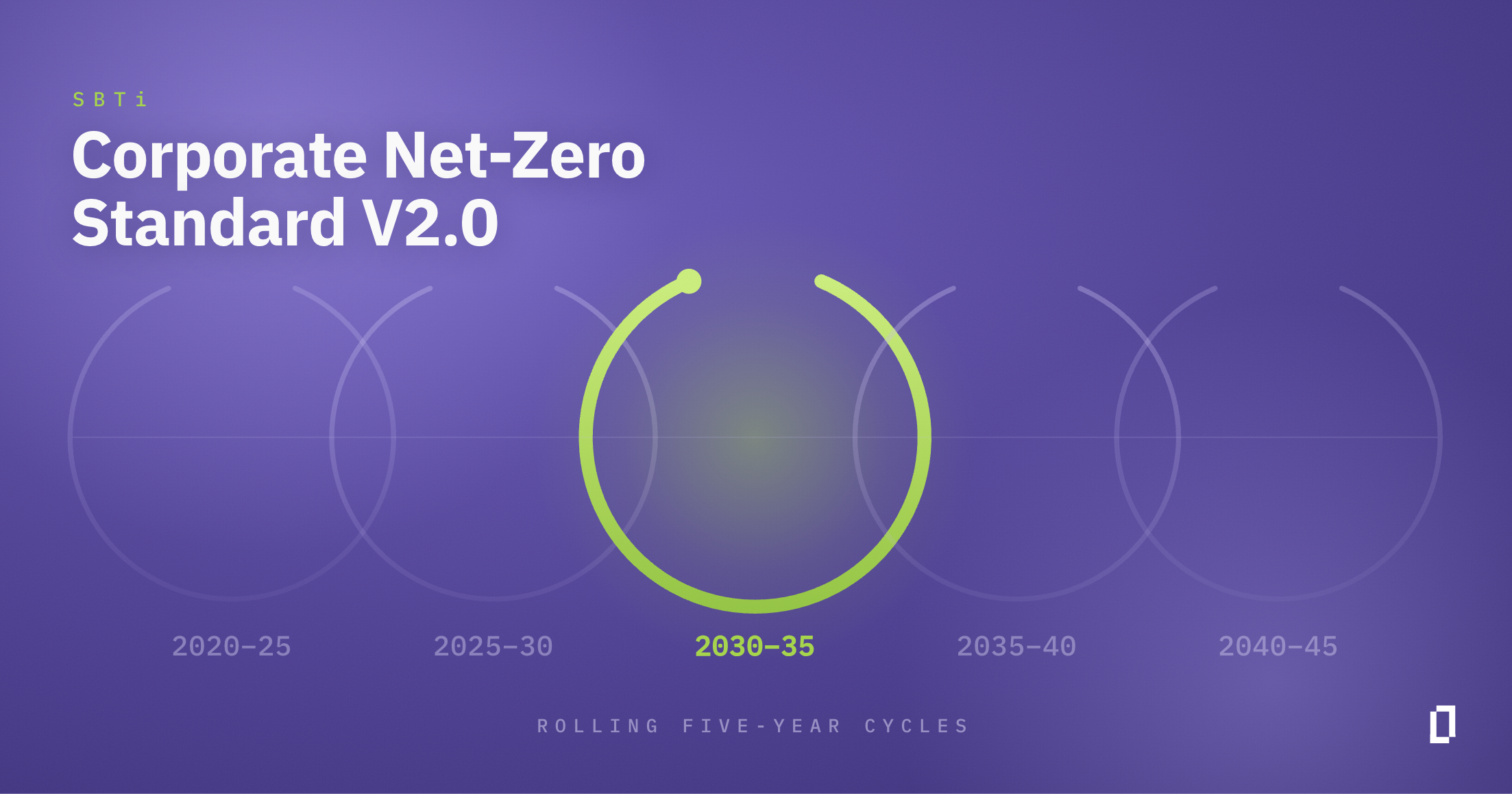

Timeline: 2025 – 2028

As per the GHG Protocol, the Land Sector and Removals Guidance (LSRG) is first up, to be published in Q4 2025 after several years of delay.

Drafts of the Corporate Standard, Scope 2, and Scope 3 standards will be shared with the public in 2026, with final publication planned for 2027.

In 2028, a new standard and guidance on Actions and Market Instruments will be published. The GHG Protocol is standardizing rules for CFOs to measure and report the verified carbon and financial impact of decarbonization projects, supply chain initiatives, and carbon credits (see IFRS sustainability disclosure standards by jurisdiction).

Practical Implications: What to Expect

- Greater clarity and consistency: Updates to the Corporate Standard, Scope 2, and Scope 3 will tighten accounting rules, close loopholes, and harmonize guidance with evolving disclosure regimes like IFRS S2 and the EU’s CSRD. This means less flexibility in interpretation and stronger comparability across companies.

- Increased scrutiny of Scope 3 and market claims: The revisions will address longstanding challenges in value chain accounting and the use of instruments like carbon credits and renewable energy certificates. For corporates, this signals more robust requirements around data quality, boundaries, and credible claims, which are critical for target-setting and building investor confidence.

- Transition, not disruption: Current standards stay in effect until new ones are published, with adoption timelines likely phased in by disclosure programs and regulators. Companies that already align closely with the GHG Protocol will face fewer surprises, but those relying on interpretive flexibility in Scope 2 or broad estimates in Scope 3 may need to adjust systems and processes.

What Leaders Should Do Now to Prepare

For CSOs and CFOs, the upcoming GHG Protocol update signals climate disclosure is maturing in line with investor expectations and global regulation. Forward-thinking business leaders should anticipate and prepare for these changes in order to edge out their competitors in capital markets and strengthen trust amongst their stakeholders.

A decisive decade for climate action can also be your decisive decade for credible disclosure.

Leaders can prepare today in four key ways:

-

Auditing Current Practices: Assess how closely your reporting aligns with likely updates, especially on Scope 2 and Scope 3. Identify areas where assumptions, estimates, or accounting choices may face challenges under stricter rules.

-

Engaging your Board and Governance Committee: Treat the upcoming GHG Protocol revisions as a financial governance issue, not just a sustainability one. Ensure climate-related disclosures are integrated into risk management and financial oversight.

-

Investing in Data and Supplier Engagement: Improve emissions data quality and build strong supplier engagement processes now. That way, your organization can adapt quickly once revisions are finalized.

-

Staying Updated with the Process: Subscribe to GHG Protocol updates, attend webinars, and monitor draft releases when they’re out for public consultation. Having an early idea of how the guidance will shape up will allow you to anticipate risks and opportunities for your company as final standards are issued. This works hand-in-hand with the earlier points, giving you ample time to get ready.

By preparing effectively for these changes, companies can solidify their leadership roles in sustainability and confidently present themselves as forward-thinking, environmentally responsible players in their industries.

For one, the GHG Protocol’s upcoming Land Sector & Removals Guidance is set to redefine how companies account for land-use, insetting, and removals — with major implications for food & beverage, agriculture, retail, forestry, and consumer goods.

In case you need to zoom into the LSRG, watch our webinar we recorded last week with experts from the SBTi, Kellanova, and Trellis, to understand what’s changing, how it affects Scope 3 and supply chain disclosures, and what credible action looks like in 2025 and beyond. Stay ahead of compliance, avoid greenwashing risks, and future-proof your climate strategy.