Summary

-

Preparation must start now: Although Group 2 and 3 companies’ first AASB S2 reports are due in 2027–2028, credible emissions data, assurance, and strategy work must begin well in advance.

-

Early movers gain strategic advantage: Companies that start early secure auditor availability, reduce compliance risks, and strengthen credibility with investors and stakeholders.

-

Readiness varies, but destination is the same: Whether starting from scratch or refining mature processes, all companies must be ready to deliver assured, transparent climate disclosures by FY27.

If you’re a Group 2 or 3 company under the new AASB S2 climate disclosure rules, you might think you have the luxury of time. After all, your first public climate report isn’t due until the 2027 financial year. But here’s the truth: by the time you reach that date, you’ll already need credible, assured emissions data. Which means the clock isn’t starting in 2027 – it’s starting now.

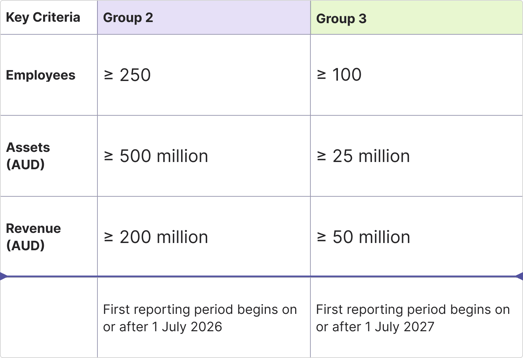

To know if an entity falls into Group 2 or Group 3 under AASB S2, it needs to check if it meets at least 2 out of 3 size criteria (listed below) at the end of a financial year.

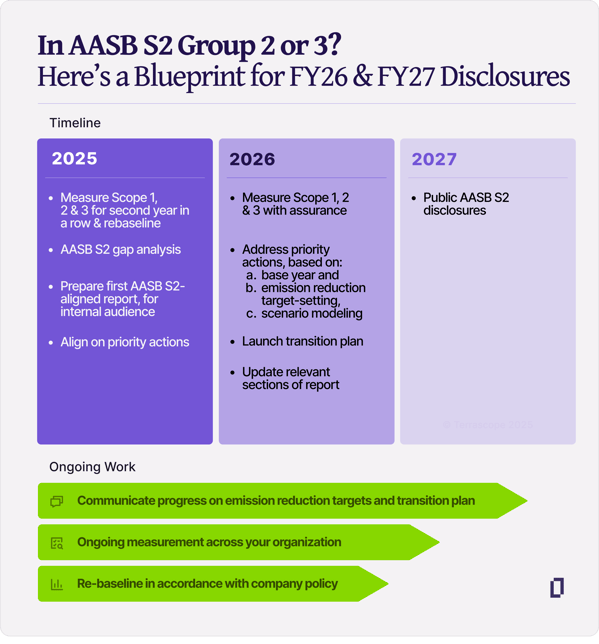

The runway is shorter than it looks

The reporting deadline may seem far away, but it’s an extensive and whole-of-organisation journey to get there, with a lot of stakeholder engagement. In FY25, you should already be measuring Scope 1, 2, and 3 emissions and defining or refining your baselines. By FY26, you should aim for third-party assurance, emission-reduction targets, scenario modelling, and a transition plan. Come FY27, that first public AASB S2 disclosure will be in the spotlight. Starting now means building capacity at a sustainable pace, not cramming a multi-year learning curve into your final 12 months.

Getting ahead of the curve pays dividends beyond meeting regulations. Early movers lock in auditor availability and avoid the last-minute bottlenecks we’ve already seen for Group 1 and 2 companies. They also build credibility with investors, boards, and customers by showing they take climate risk and opportunity seriously. This is more than a box-ticking exercise. Scenario modeling and transition planning can uncover risks in your supply chain, flag cost exposures like carbon pricing, and identify opportunities for efficiency and innovation. Companies that start early often discover they can turn compliance into a competitive advantage.

Different starting points, same destination

Not every Group 3 company is starting from the same place. If you’ve never measured before, this is the moment to get your first Scope 1, 2, and 3 footprint. If you’ve been tracking in spreadsheets, moving to a purpose-built platform will save lean sustainability teams countless hours, reduce errors, and make assurance smoother. And if you’re already ahead, this is the time to deepen your governance story, refine your targets, and prepare for ongoing re-baselining. Wherever you are today, the destination is the same: a confident, compliant public disclosure in FY27 that tells your climate story clearly and credibly.

Some companies will delay, thinking they’ll save effort by starting later. But the reality is that compressed timelines lead to rushed data collection, higher assurance risks, and weaker narratives that won’t withstand scrutiny from investors or regulators. Late starters risk being overshadowed by competitors who are already publishing transparent, assured climate data. The companies who win here are the ones who make early preparation part of their strategy.

How Terrascope can help

We’ve helped companies at every stage of the journey. For newcomers, we make measurement and self-assessment straightforward. And for advanced teams, we support in-house sustainability teams with transition planning, assurance readiness, scenario modeling, risk and opportunity identification and net zero strategy to sharpen your public disclosure for FY27 and beyond.

The AASB S2 deadline won’t move. But you can. And the sooner you do, the more control you’ll have over your competitive positioning in a low-carbon economy. Sign up for a complimentary workshop today on AASB S2 compliance - find out how you can be unlocking emissions transparency today.