.png)

Summary

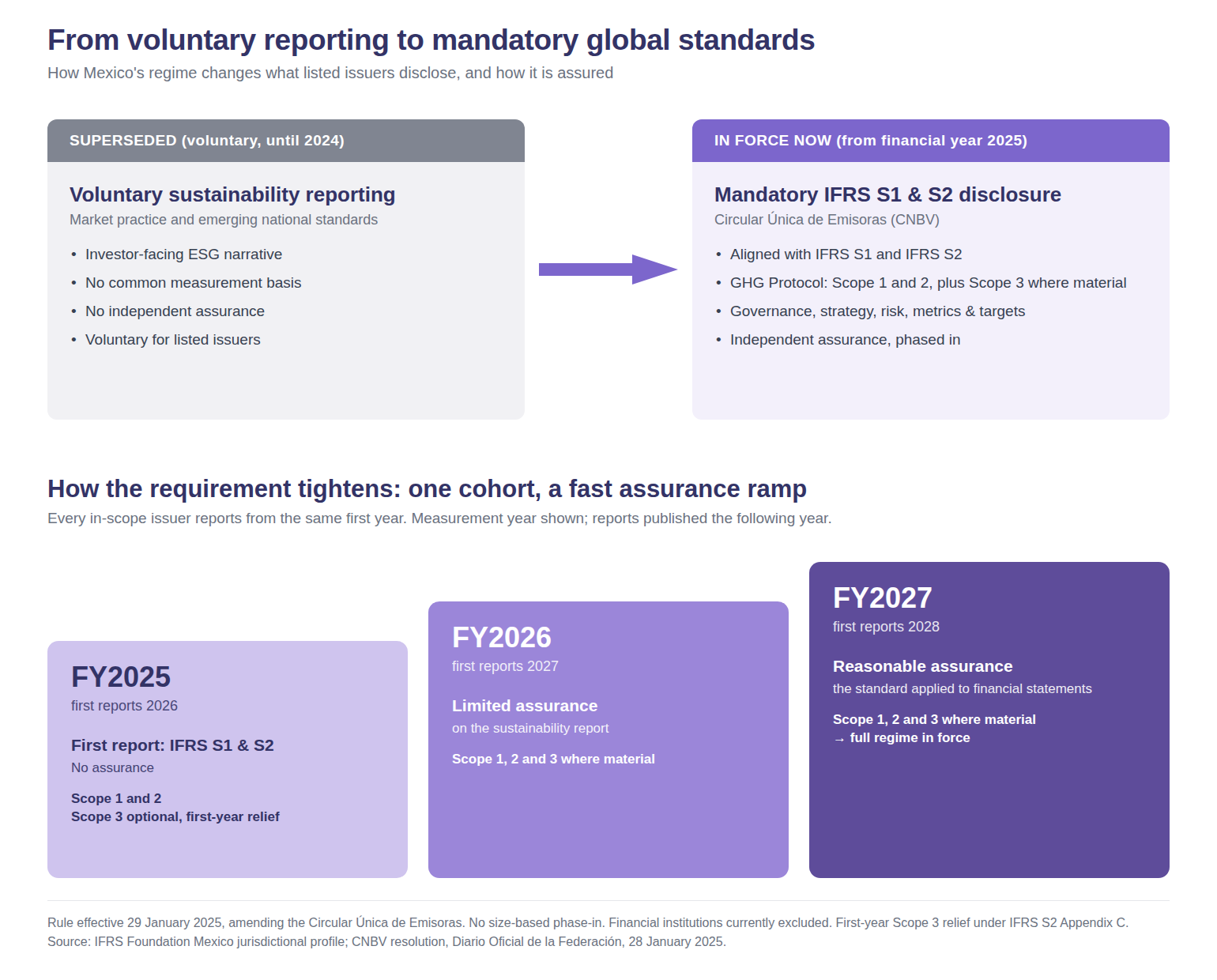

- Mexico's National Banking and Securities Commission requires listed non-financial issuers to disclose sustainability and climate information under IFRS S1 and IFRS S2, effective 29 January 2025.

- Measurement starts with the 2025 financial year, and first reports are published in 2026 alongside the annual financial statements.

- Every listed non-financial issuer is in scope, with no size-based phase-in; financial institutions are excluded while the regulator develops separate requirements for them.

- Assurance escalates quickly: first reports do not require assurance, and then limited assurance from 2027, and reasonable assurance from 2028. Companies are advised to prepare audit-ready data from the very first cycle.

Mexico's climate disclosures at a glance

| Regulator | National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores), which supervises the securities market. Affected issuers list on the Mexican Stock Exchange (Bolsa Mexicana de Valores) |

| Standard |

IFRS S1 and IFRS S2, the sustainability and climate standards from the International Sustainability Standards Board, incorporated by reference into the General Provisions Applicable to Securities Issuers (the Circular Única de Emisoras) |

| Companies in scope |

All listed non-financial issuers registered in the National Securities Registry (Registro Nacional de Valores), domestic and foreign. Financial institutions, states, and municipalities are excluded |

| Estimated population | No official count published. In-scope issuers represented 86% of the market capitalisation of the IPC, the main index of the Mexican Stock Exchange, at the end of the first quarter of 2025 |

| First reporting year | Financial year 2025, with first reports published in 2026 alongside the annual financial statements |

| Scope 3 required | Yes, where material, from the financial year 2026 report. The IFRS S2 first-year transition relief allows Scope 3 to be omitted from the financial year 2025 report |

| Assurance | None on 2026 reports; limited assurance on 2027 reports; reasonable assurance from 2028 reports, under the International Standard on Sustainability Assurance 5000 and the International Standard on Assurance Engagements 3000 (Revised) |

| Penalty regime | Not specified in the rule |

From voluntary to mandatory

Mexican listed companies reported sustainability information voluntarily for years before the rule made it mandatory.

-

Voluntary market practice. Larger issuers reported using frameworks such as the Global Reporting Initiative, with no common measurement basis and no independent assurance.

-

2024, a national standard-setter steps in. The Mexican Financial Reporting and Sustainability Standards Board published its first sustainability standards in May 2024, developed to converge with the International Sustainability Standards Board's global baseline.

-

2025, the regulator mandates the global standards. The National Banking and Securities Commission amended the General Provisions Applicable to Securities Issuers to require listed issuers to report under IFRS S1 and IFRS S2 directly.

The shift moves Mexican issuers from a qualitative sustainability narrative to a standardised disclosure with measured greenhouse gas emissions and, within three reporting cycles, reasonable assurance.

What Mexico's climate disclosure rules require

In-scope issuers must prepare a sustainability report in accordance with IFRS S1 and IFRS S2, published at the same time as the annual financial statements.

-

IFRS S1 (General Requirements): the disclosure architecture. Issuers report material information about sustainability-related risks and opportunities that could reasonably be expected to affect their cash flows, access to finance, or cost of capital over the short, medium, and long term.

-

IFRS S2 (Climate-related Disclosures): the climate-specific requirements, built on the four pillars of governance, strategy, risk management, and metrics and targets, covering Scope 1, Scope 2, and, where material, Scope 3 greenhouse gas emissions.

-

The Greenhouse Gas Protocol as the measurement standard: IFRS S2 paragraph 29(a)(ii) requires emissions to be measured in accordance with the Greenhouse Gas Protocol Corporate Accounting and Reporting Standard (2004).

What the first report has to contain. Scope 1, Scope 2, and material Scope 3 emissions are the steady-state requirement under IFRS S2. The transition provisions in Appendix C of IFRS S2 let an issuer omit Scope 3 in its first annual reporting period, and Mexico adopted the IFRS S1 and IFRS S2 reliefs without modification. The financial year 2025 report can therefore carry Scope 1 and Scope 2 alone, with Scope 3 where material joining from the financial year 2026 report.

Because the Commission incorporated the standards by reference, IFRS S1, IFRS S2, and future standards from the International Sustainability Standards Board apply as issued. The sustainability report is a separate report published together with the financial statements, on the same annual filing cycle issuers already use.

Which companies are in scope

Every listed non-financial issuer supervised by the National Banking and Securities Commission reports under the rule, with no phase-in by company size.

Issuers with securities registered in the National Securities Registry, both domestic companies and foreign issuers listed in Mexico, are in scope . Domestic issuers report under IFRS S1 and IFRS S2. Foreign issuers report under IFRS S1 and IFRS S2 or, alternatively, under the sustainability disclosure standards of their jurisdiction of origin; an issuer taking the second route states that the information is not presented in accordance with ISSB Standards, or explains the interoperability or equivalence of what it reports with ISSB Standards.

Unlike phased regimes that start with the largest companies, Mexico brings every in-scope issuer into reporting for the same first year: the 2025 financial year.

Two groups sit outside the current scope. Financial institutions are excluded for now, and the regulator has stated it is analysing how to set requirements for them, which points to a later extension. States, municipalities, and private entities without public accountability are outside the rule entirely.

Terrascope's analysis of the supply chain implications: the rule addresses issuers, not their suppliers. However, once a Mexican issuer reports Scope 3 emissions, its significant suppliers become data sources, whether they sit in Mexico, or elsewhere. Suppliers in transport and distribution, manufacturing, and food value chains should expect emissions data requests from their Mexican customers even before their own jurisdictions require reporting.

Key dates and milestones

|

Reporting cycle |

Measurement year |

Report published |

GHG emissions required |

Assurance |

|---|---|---|---|---|

| First report under IFRS S1 and IFRS S2 |

Financial year 2025 | 2026 | Scope 1 and Scope 2, with Scope 3 optional under the IFRS S2 first-year transition relief |

None |

| Second cycle |

Financial year 2026 | 2027 | Scope 1, Scope 2, and Scope 3 where material | Limited assurance |

| Third cycle onwards | Financial year 2027 | 2028 | Scope 1, Scope 2, and Scope 3 where material | Reasonable assurance |

The rule took effect on 29 January 2025, the day after publication in the Official Gazette of the Federation (Diario Oficial de la Federación). Reasonable assurance, the same standard auditors apply to financial statements, applies to reports published from 2028, covering the 2027 financial year.

One timing point for the first cycle. Same-time publication with the financial statements is the standing requirement, subject to the transition relief for the first annual reporting period in paragraph E4 of IFRS S1. That relief allows the first sustainability report to follow the financial year 2025 financial statements rather than accompany them. Mexico added no extensions and no modifications to the IFRS S1 and IFRS S2 reliefs.

Why this matters beyond Mexico

Mexico's rule reaches past its own exchange, both through supply chains and as a regional signal.

-

Supply-chain ripple across North America. Mexican issuers sit at the centre of North American manufacturing, automotive, and agricultural value chains. Their Scope 3 obligations turn into emissions data requests for suppliers and trading partners in the United States, Canada, and beyond, regardless of what those partners' home regulators require. Companies that supply Mexican listed groups become part of a disclosure they do not file themselves.

-

Regional convergence in Latin America. Mexico now sits alongside Brazil, whose securities regulator adopts IFRS S2-aligned reporting phased from 2026, and Chile, whose financial market regulator has folded sustainability disclosure into its rules. A company with entities across several Latin American markets can build one IFRS S2-aligned inventory and reuse it rather than rebuilding for each.

- Capital-markets precedent. By writing the global standards into its listing rules with a firm assurance ramp, Mexico gives international investors a familiar, comparable disclosure from Latin America's second-largest economy, and raises the bar for issuers competing for cross-border capital and nearshoring investment.

How companies should prepare

Issuers are measuring the 2025 financial year now, and the assurance requirement is only two cycles behind. The preparation work is the same across the reporting universe.

-

Establish your greenhouse gas inventory. Build Scope 1, 2, and 3 measurement on the Greenhouse Gas Protocol Corporate Accounting and Reporting Standard (2004), the basis IFRS S2 requires. Scope 3 categories take the longest to source, so the first-year relief is preparation time, not a reason to wait.

-

Map your value-chain exposure. Identify which suppliers and customers feed your material Scope 3 categories, and which of your customers are Mexican issuers that will request your data. Both directions shape the numbers you report.

-

Build assurance-ready processes early. Reasonable assurance, arriving on 2028 reports, is the same bar auditors apply to financial statements. Methodology documentation, source-data traceability, and role-based review need to be in place during measurement, well before the engagement starts.

- Build on the frameworks you already use. Issuers that have reported under the Global Reporting Initiative, the four-pillar climate structure, or CDP already hold much of the underlying data, which maps onto IFRS S1 and IFRS S2 rather than starting from zero.

Your first climate audit

Preparing for your first limited assurance engagement under Mexico's rules from 2027? Download A Practical Guide to Your First Climate Audit for a step-by-step walkthrough of what external auditors expect.

How Terrascope can help

Terrascope's AI-powered platform helps companies operating in Mexico and across the Americas move from baseline emissions data to audit-ready disclosures, including Dyno Nobel, who achieved limited assurance over their global Scope 1 and Scope 2 emissions, 1.6 million tCO2e across five continents, one year ahead of mandate.

-

Scope 1, 2, and 3 emissions measurement. Integrations pull emissions data from your source systems monthly, so your inventory stays current across every entity and business line in scope.

-

Audit-ready reporting. Audit Trail makes every figure traceable from data entry to disclosure, with assurance-provider access built in for the limited and reasonable assurance engagements arriving from 2027 and 2028.

-

Supply-chain intelligence. Analytics shows you where your Scope 3 hotspots sit before the disclosure deadline, so the first-year relief becomes reduction-planning time.

- Multi-framework alignment. ISSB Reporting drafts your IFRS S1 and IFRS S2 disclosures from your measured data, reviewed by your team, ready for the sustainability report you publish with your financial statements.

Are you ready to get ahead of Mexico's IFRS S1/S2 requirements?