Summary

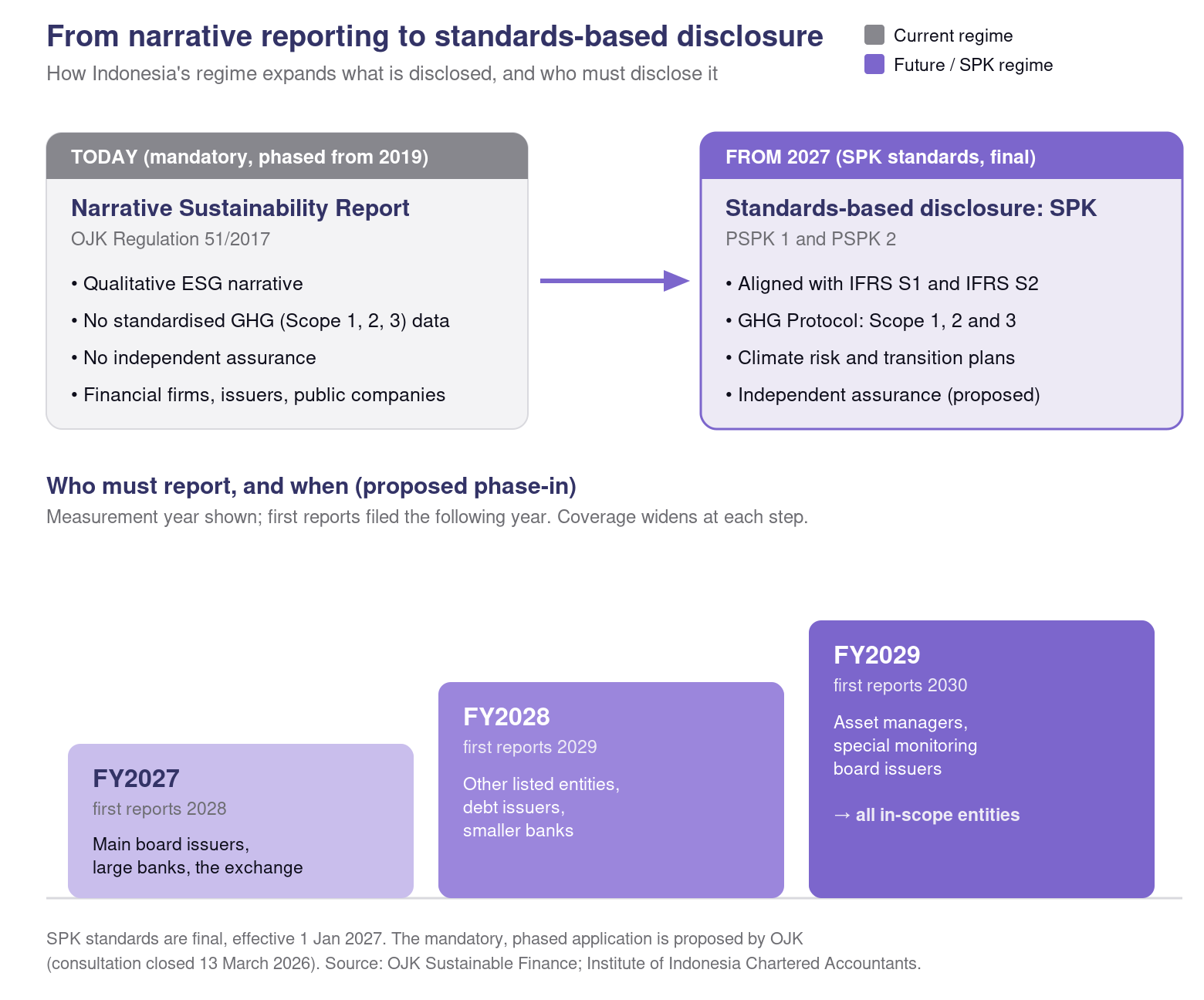

- Sustainability reporting is already mandatory under OJK Regulation 51/POJK.03/2017, but in narrative form; the new Sustainability Disclosure Standards (PSPK 1 and PSPK 2) replace it with standards-based disclosure aligned with IFRS S1 and IFRS S2.

- The standards take effect on 1 January 2027, and a draft OJK regulation would phase in the mandatory standards-based regime from FY2027 through FY2029. Information is still under consultation and subject to change.

- The first wave covers main board issuers, large banks, and the stock exchange, before extending to additional listed entities, debt issuers, and smaller banks.

- Companies that build a Scope 1, 2, and 3 inventory now, ahead of the proposed independent assurance requirement, will be ready when their phase begins.

Indonesia climate disclosure at a glance

| Regulator | Financial Services Authority (Otoritas Jasa Keuangan, OJK) for the reporting mandate; Sustainability Standards Board of the Institute of Indonesia Chartered Accountants (DSK IAI) as standard-setter |

| Standard |

Moving from a narrative Sustainability Report (mandatory since 2017 under OJK Regulation 51/POJK.03/2017) to the standards-based Sustainability Disclosure Standards (SPK) from 2027: PSPK 1 (general requirements, aligned with IFRS S1) and PSPK 2 (climate-related disclosures, aligned with IFRS S2) |

| Companies in scope |

Phased (proposed): main board issuers, large banks, and the stock exchange first, extending to additional listed entities, debt issuers, and smaller banks through 2028 and 2029 |

| First reporting year | SPK effective 1 January 2027; phased OJK mandate begins 2027 (proposed) |

| Scope 3 required | Yes, under PSPK 2, which mirrors IFRS S2; commencement timing proposed in the draft regulation, subject to consultation |

| Assurance | Mandatory independent assurance proposed in the draft regulation; phasing and assurance levels subject to consultation |

| Penalty regime | Existing sustainability reporting carries administrative sanctions under OJK Regulation 51/POJK.03/2017; the new mandate's enforcement provisions are subject to consultation |

Sustainability reporting is already mandatory in Indonesia: since 2017, the Financial Services Authority (Otoritas Jasa Keuangan, OJK) has required financial services institutions, issuers, and public companies to file an annual narrative Sustainability Report.

Indonesia is now moving that obligation to a standards-based regime built on the national Sustainability Disclosure Standards (Standar Pengungkapan Keberlanjutan, SPK), which take effect on 1 January 2027 and align with IFRS S1 and IFRS S2.

A draft OJK regulation, out for public consultation between 12 February and 13 March 2026, would make this standards-based reporting mandatory on a phased basis, starting with the FY2027 reporting period (first reports published in 2028) for main board issuers, large banks, and the stock exchange, placing Indonesia alongside Singapore, Malaysia, and Australia among Asia-Pacific economies adopting the ISSB global baseline.

What Indonesia's climate disclosure rules require

Indonesia's Sustainability Disclosure Standards require companies to disclose sustainability-related and climate-related risks and opportunities that affect enterprise value, following the same four-pillar structure used across IFRS-aligned regimes.

-

PSPK 1 (general requirements): Sets the conceptual foundations, reporting location, and timing for sustainability-related financial disclosures, organised around the four content areas of governance, strategy, risk management, and metrics and targets. It mirrors IFRS S1.

-

PSPK 2 (climate-related disclosures): Focuses on climate-specific risks and opportunities, including greenhouse gas emissions, transition exposure, and climate resilience. It mirrors IFRS S2.

-

GHG Protocol as the measurement standard: Because PSPK 2 follows IFRS S2, greenhouse gas emissions are measured using the GHG Protocol Corporate Accounting and Reporting Standard (2004), the basis IFRS S2 mandates at paragraph 29(a)(ii).

The draft OJK regulation also proposes that in-scope organisations develop transition plans addressing their sustainability-related risks and opportunities, with the disclosures subject to mandatory independent assurance.

Who is in scope

The draft OJK regulation applies to financial sector entities, issuers, and public companies, phased by size and market segment so the largest entities report first.

What applies today: Indonesia has required financial services institutions, issuers, and public companies to file an annual Sustainability Report (Laporan Keberlanjutan) since OJK Regulation 51/POJK.03/2017 took effect, phased in by institution type and size. That report is narrative, covering environmental, social, and governance performance. It does not require standards-based climate disclosure, structured Scope 1, 2, and 3 accounting, or independent assurance.

What changes under the SPK: The new regime keeps the obligation and raises the bar of what reports contain, moving to the IFRS-aligned PSPK 1 and PSPK 2 standards. Companies already filing under OJK Regulation 51/POJK.03/2017 hold the governance and data foundation to make the shift.

First phase (proposed, 2027)

-

Main board issuers: Companies listed on the main board of the Indonesia Stock Exchange.

-

Large banks: Major banking institutions supervised by OJK.

-

The stock exchange: The market operator itself.

Later phases (proposed, 2028 to 2029)

-

Additional listed entities and debt issuers: Companies on other market segments and issuers of listed debt instruments.

-

Smaller banks and asset managers: Remaining banking institutions and investment managers, given additional time to build data systems and governance.

Key dates and milestones

|

Milestone |

Measurement Year |

First Reporting Date |

|---|---|---|

| SPK (PSPK 1 and PSPK 2) take effect | FY2027 | 2028 (for FY2027) |

| Phase 1 mandate: main board issuers, large banks, stock exchange (proposed) | FY2027 | 2028 (proposed) |

| Phase 2 mandate: additional listed entities, debt issuers (proposed) | FY2028 | 2029 (proposed) |

| Phase 3 mandate: smaller banks, asset managers (proposed) | FY2029 | 2030 (proposed) |

The phasing dates carry the "(proposed)" qualifier because they come from the draft OJK regulation, whose consultation closed on 13 March 2026. The SPK effective date of 1 January 2027 is set by the standard-setter and is firm. This page will be reviewed within 30 days of the final regulation being published.

How companies should prepare

Companies operating in Indonesia can take four steps now, before their reporting phase begins.

-

Establish your GHG inventory. Build a Scope 1, 2, and 3 emissions inventory on GHG Protocol foundations, the measurement basis PSPK 2 inherits from IFRS S2.

-

Map your value-chain exposure to in-scope entities. Identify which of your customers are main board issuers or large banks reporting from 2027, because those buyers will request supplier-level emissions data.

-

Build assurance-ready processes early. The draft regulation proposes mandatory independent assurance, so document methodology, keep an audit trail, and assign role-based review from the first reporting cycle.

-

Build on the frameworks you already use. Reporting under OJK Regulation 51/POJK.03/2017, TCFD, or CDP already covers much of what PSPK 1 and PSPK 2 require.

Frequently asked questions

How Terrascope can help

Terrascope's AI-powered platform helps companies operating in Indonesia and across Asia-Pacific move from baseline emissions data to audit-ready disclosures, including Greenfields, the Indonesian dairy producer that uncovered methane emissions insights across its dairy value chain to inform its sustainability strategy.

-

Scope 1, 2 and 3 emissions measurement. Corporate carbon footprinting pipes energy data, fuel records, procurement spend and supplier data into a GHG Protocol-aligned inventory, with full audit trail from source system to disclosed figure.

-

Audit-ready reporting. Capture methodology, factor selections and version history for every emission category, with role-based assurance-provider access matched to the assurance phasing.

-

Supply-chain intelligence. Supplier engagement surfaces category-level Scope 3 hotspots across your supplier network, identifying where supplier engagement moves the disclosed number most.

-

Multi-framework alignment. Climate reporting produces a narrative report mapped to IFRS S2's disclosure requirements. See how it works on our Climate Reporting page, or join a complimentary workshop.

Need to get ahead of Indonesia's reporting requirements? Speak to a Terrascope expert today.